This article was produced by Capital Group without involvement from the Top1000funds.com editorial team.

Populism has become part of the global landscape, rooted in frustrations over inequality, stagnant mobility, and a sense that mainstream policymakers have failed to adapt to shifting economic realities.

While populist administrations often pursue policies that raise long‑term risks — slower growth, higher inflation, and elevated volatility — they can also generate short‑term support for demand, unlock space for overdue reforms, and create targeted investment opportunities in subsidised or strategically favoured sectors.

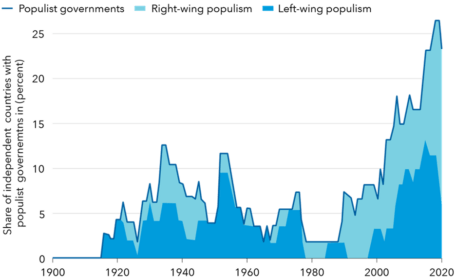

Populist governments over time

Source: Populist Leaders and the Economy, Manuel Funke, Moritz Schularick, and Christoph Trebesch, 2023

For bond markets, populist governments often push for expansionary monetary policies to stimulate growth or meet social demands, leading to lower short-term interest rates. These interventions are typically accompanied by rising long-term bond yields, as investors grow concerned about fiscal sustainability, inflation risk, and potential deficit monetisation.

This yield increase reflects more than a technical adjustment — it signals a shift in market expectations around the risk premium required to hold government debt under less predictable policy regimes. The result is a steepening yield curve, with short-term rates held down by policy and long-term rates rising in response to elevated inflation expectations and fiscal uncertainty.

With equities, populist policy shifts — such as tariffs, fiscal expansion, and regulatory interventions — create distinct winners and losers in markets, particularly where government intervention intersects with strategic sectors.

Recent developments in the US — such as golden share arrangements, public-private equity deals, and policy reversals on chip export controls — highlight how political agendas can distort capital allocation and earnings visibility. Geopolitical tensions, including China’s restrictions on AI chip purchases and threats of escalation with the US, further compound uncertainty. At the same time, proposed funding cuts to key innovation agencies risk undermining long-term growth drivers, making asset valuations more fragile in politically charged environments.

For investors, the task is not to dismiss populism outright but to navigate it selectively. Understanding the underlying forces that give rise to populist shifts is essential, as these pressures will continue to shape policy trajectories. A disciplined, sector‑aware, and time‑horizon‑conscious approach — anchored in an assessment of institutional strength and reform credibility — offers the best chance of capturing opportunities while managing the structural risks that accompany populist governance.

This insight is part of our broader analysis on how today’s global shifts are impacting investment opportunities – a dynamic we call The Great Global Restructuring. Find out more.

Statements attributed to an individual represent the opinions of that individual as of the date published and may not necessarily reflect the view of Capital Group or its affiliates. This communication is intended for the internal and confidential use of the recipient and not for onward transmission to any other third party. This communication is of a general nature, and not intended to provide investment, tax or other advice, or to be a solicitation to buy or sell any securities. All information is as at the date indicated and attributed to Capital Group unless otherwise stated. While Capital Group uses reasonable efforts to obtain information from third-party sources that it believes to be accurate, this cannot be guaranteed.

This communication is issued by Capital International Management Company Sàrl (CIMC), unless otherwise stated, which is regulated by the Luxembourg CSSF – Commission de Surveillance du Secteur Financier.

In Switzerland, this communication is issued by Capital International Sàrl, authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA).

In the UK, this communication is issued by Capital International Limited, authorised and regulated by the UK Financial Conduct Authority.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company. All other company names mentioned are the property of their respective companies.

© 2026 Capital Group. All rights reserved.

Leave a Comment

You must be logged in to post a comment.

Login