This article was produced by Capital Group without involvement from the Top1000funds.com editorial team.

Towards the end of 2024, one of our key economic themes was that the US and Europe seemed to be on divergent growth paths. Europe was becoming more fragile, both cyclically and structurally. Meanwhile, the US remained, what we called a grower economy, benefitting from both cyclical and structural resilience.

Our view was that if nothing changed, this trend was likely to continue. However, since publishing the paper, a lot has changed. Donald Trump’s return to the White House, and the announcement of reciprocal tariffs that were more draconian than anyone expected, pose a significant risk to growth and increase the potential for US recession in 2025.

At the time of writing, these reciprocal tariffs have been paused for 90 days. While the market has welcomed this development, it is worth noting tariffs are, for now, only paused, and, importantly, the political uncertainty resulting from the constantly shifting trade landscape is in itself likely to have a negative effect on investment and consumption.

On the other hand, Europe’s response of more fiscal spending helps support growth, partly offsetting the drag from tariffs.

From that perspective, we observe the dynamic between the two economies appears to have shifted from one of divergence to potential convergence, with a revitalised Europe and heightened risks that potentially lead the US to slower growth.

For investors, it is easy to get distracted by the headlines but a lot of what is happening is ultimately noise. We believe fixed income investors should continue to focus on the long-term fundamentals. Yields, which are a good proxy for long-term total returns, remain high and can therefore absorb a significant amount of near-term volatility.

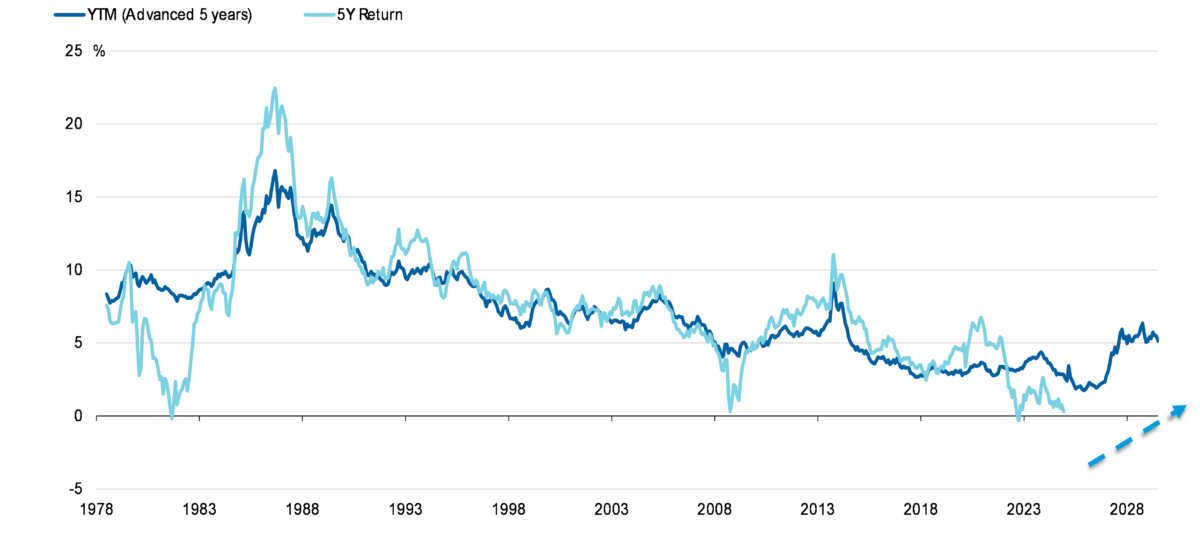

The power of yield

Past results are not a guarantee of future results.

Data from 31 January 1973 to 31 December 2024 and in US dollar terms. Index used: Bloomberg US Corporate Total Return Index. Source: Bloomberg. YTM: Yield to Maturity

As simple as it sounds, yields are a proxy for future total returns. For example, looking at investment-grade corporate bond yields, history shows the correlation between starting yield and total return over the next five years has been extremely high.

Today, depending on the quality of issue, fixed income markets offer yields of between 4% and 8% across sectors and locking in these yields offers good value over the long term. Meanwhile, high-quality assets should benefit from duration in a recessionary scenario where rates are expected to fall and also provide diversification.

While credit spreads have widened sharply, they remain below long-term historical averages. Similarly, the differential between high yield and investment grade credit has widened significantly, but this has been from historically very tight levels. Consequently, the spread is now around the historical average. However, the likelihood of ongoing uncertainty could lead to further widening, with dispersion also likely to increase. For this reason, we remain defensively positioned with a bias towards higher quality.

Importantly, we have dry powder in portfolios and are ready to capitalise on any opportunities as valuations become more attractive.

The constantly changing macroeconomic backdrop underlines the importance of taking a long-term view. We believe investors should focus on idiosyncratic opportunities that can take advantage of the dispersion created and that are more resilient in this environment. A good example of such are electric utilities, which are solid defensive issuers not directly impacted by tariffs.

One area of opportunity is emerging markets (EM), specifically local currency bonds in Latin America and Asia. Fundamentals across many EM economies remain relatively healthy with a good ability to service debt thanks to continued reserves accumulation. Inflation has moderated substantially from 2022 peaks and is generally on a downward trend amid continued restrictive monetary policy stances. The impact from tariffs should weaken inflation further. Fiscal indicators are generally the weak spots, but most of the major EMs have lengthened the maturity profile of their debt and are issuing more now in local currency.

This is a pivotal time for the global economy, with many certainties of the past 40 years or more seeming to be in flux. The outcome, remains highly uncertain and to an extent binary, and the investment implications for this structural shift are not yet clear. We therefore continue to position portfolios based on the underlying fundamentals – which in our view remain strong, particularly in corporate credit and many emerging markets – while closely monitoring the structural developments.

To read more about Capital Group’s fixed income capabilities, click here.

Leave a Comment

You must be logged in to post a comment.

Login