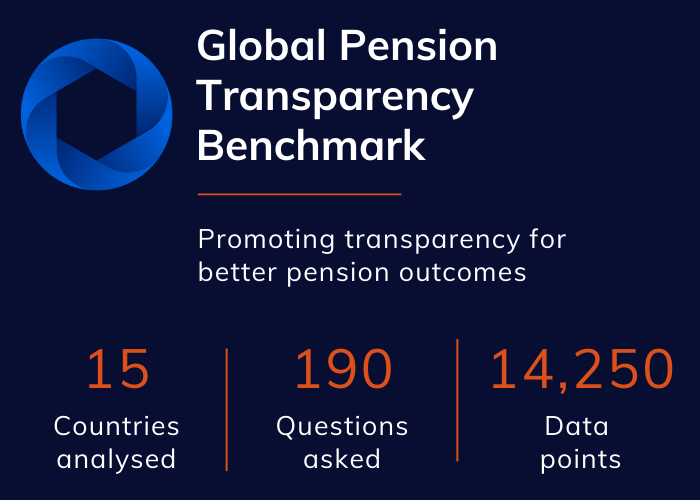

GPTB refines process to promote, even greater, transparency

Increased scrutiny on the transparency of disclosures is driving measurable improvements among some of the world’s largest asset owners, as refinements to the Global Pension Transparency Benchmark methodologies and board oversight boost attention on transparency.