New research investigates the systemic impacts of the large and growing superannuation industry in Australia highlighting two main concerns, that may differ from what you expect, and drawing conclusions for other evolving defined contributions systems.

The Conexus Institute recently released a report titled Systemic impacts of ‘big super’. The full 85-page report can be found here, and shorter summary version here. The research investigates the implications for the broader Australian economy, financial markets and population of what has become a large superannuation (i.e. pension) system containing some very large funds.

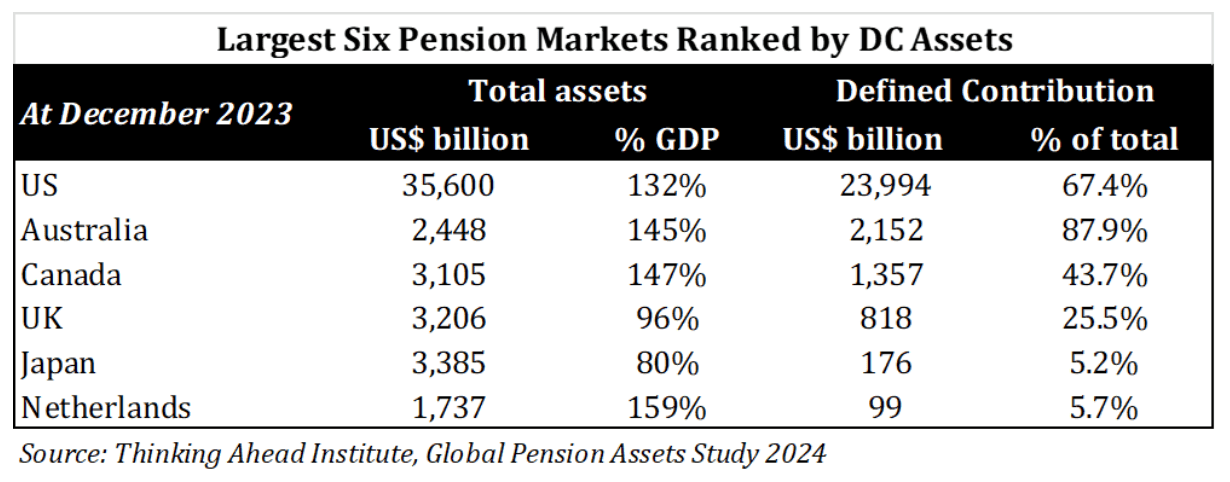

As at September 2024, assets in the Australian super industry stood at A$4.1t ($2.8 trillion), 150 per cent of GDP. The biggest fund (AustralianSuper) had A$355 ($246) billion in assets. The Australian system is also substantially (around 90 per cent) defined contribution (DC). In fact, it is the second largest DC system in the world behind the US (see table).

Our broad-ranging report considered the benefits, risks and issues arising from big super. The overall conclusion is that Australia’s super system is a boon. It has facilitated the creation of a large pot of retirement savings that is being professionally managed, and brings benefits related to improved stewardship of capital and broadening out of available funding sources in the economy.

Our broad-ranging report considered the benefits, risks and issues arising from big super. The overall conclusion is that Australia’s super system is a boon. It has facilitated the creation of a large pot of retirement savings that is being professionally managed, and brings benefits related to improved stewardship of capital and broadening out of available funding sources in the economy.

We highlight two main concerns that may differ from you expect. The first is that super exposes members to economic and market risk, with a 70/30 growth/defensive mix being typical. While we consider this entirely appropriate as it boosts expected retirement outcomes, it is not without risk. Growth assets are likely, but not guaranteed, to deliver over the long run. Second, the operational infrastructure of the industry (administration, etc) appears underdeveloped. This is causing issues in areas like member servicing, and will require considerable effort, cost and time to upgrade. It also leaves the maturing system underprepared to develop and deliver a more personal tailoring in the retirement phase.

Our report considers a variety of other issues, including the implications of significant FX exposure, service supplier concentration, vulnerability to scams, effects arising from herding of investment behaviour, super proving an unreliable source of funding for a sector, prospect of loss of confidence and trust, and effects arising from increasing fund size for governance, management, culture and ability to exert influence. We see scope for a range of impacts, but conclude it unlikely that any of these impacts reach the hurdle of ‘systemic’ in nature.

We also consider whether super could be a source or magnifier of systemic stress in the Australian economy and/or financial system, including the potential for a system-wide liquidity squeeze or a run on a major fund. We argue that super is an unlikely source of systemic stress, and could either be a magnifier or dampener of stresses that emerge from other sources.

Here we stand somewhat at odds with commentators – including the IMF – which has expressed concerns over exposure to liquidity risk in a DC system offering redemption-at-call while carrying investments in illiquid assets and currency hedges (which can give rise to margin calls). In the remainder of this article, we unpack why we have much less elevated concerns over the issue, and reflect on the implications for pension system design.

Our limited concern relates to the settings of the Australian system and how super funds have set their portfolios. First, in a DC pension system the members bear the risk. Super funds are also not permitted to leverage. There are no guarantees to force selling in response to poor market returns.

Second, the experience is that the vast majority of members have remained inactive – even in the face of developments such as the Global Financial Crisis of 2008-9 (“GFC”) or COVID. The assets are preserved in the super system until retirement, prior to which members are only able to switch funds and investment options. Meanwhile, the system as a whole is in inflow, and is projected to remain so for around another decade. This greatly reduces the potential for significant outflows from the system overall, although the possibility of outflows from particular funds remains.

Third, very few super funds hold more than 30 per cent in illiquid assets while currency hedges are about 16 per cent of assets for large super funds, which significantly limits the potential for a liquidity crisis. Consider what would happen if a fund with 30 per cent illiquid assets suffered an outflow of (say) 10 per cent of assets under management. The initial response would be to sell their liquid assets, resulting in the illiquid assets moving from 30 per cent to one-third (i.e. 30/90) weight. The result would be a modestly out-of-shape portfolio, while individual funds are not significant enough to disrupt markets. So no big issue. We run analysis that combines high illiquid asset exposure and currency hedges with fund outflows and market declines, and find it hard to build a plausible scenario that ends in disaster.

Nevertheless, members of a fund in outflows may suffer some losses as a consequence of their fund being a forced seller of assets, and needing to tidy up an untidy portfolio in the fullness of time. But this is hardly a systemic event. Further, from a system perspective, those on the other side of the trades will benefit.

Fourth, institutional settings provide further protection. The regulator requires funds to have detailed liquidity management processes and plans in place. If worse comes to worse, the regulator can suspend the requirement that a fund meets redemptions. And we feel confident that the authorities would take whatever action is needed if liquidity pressures in super amounted to a systemic threat.

In sum, there are lots of gates to go through before super causes a liquidity event of systemic importance. Not impossible, but highly unlikely.

How might super funds behave in an economic and market crisis? On one hand, they could magnify the stress by joining a pile-on to sell assets or withdrawing capital from some sectors. On the other hand, rebalancing activities and the opportunity to pick up cheap assets may encourage them to step up to the plate and provide funding where it is most needed. Indeed, this is how super behaved during the GFC. How members react to the crisis (i.e. switching activity) may also have effects. Whether super acts as a magnifier or dampener of system stress will depend on how the situation unfolds.

The main message is that the specifics of both the pension system and the circumstances are important. In DC systems, the members bear the risk. Here pension funds act as a conduit to distribute the effects of systemic stress around the economy. Whether pension funds themselves exacerbate the situation depends on the system settings. In the Australian system, risks are limited by the fact that it is a partly closed system (at least in accumulation) in inflow with mainly inactive members, no leverage, exposure to illiquidity and derivatives being kept to manageable levels, and regulatory settings that help to keep everything in check. These features need not apply in other DC systems.

In DB pension systems, the liabilities are typically well-defined undertakings with the sponsor bearing the risk. Dynamics such as the management of mark-to-market funding ratios and use of derivatives to manage exposures can be at play. The ‘crisis’ in the UK system during 2022 is a salutary example or how these features can have systemic implications. Leverage may also be used, which is a feature in the Canadian system. Political considerations may also loom large, with US public pension plans being a case in point. In some systems, the assets are concentrated within one major fund, e.g. Korea, Norway and Singapore.

The bottom line is that the specific settings of a pension system matter for its potential to have systemic impacts that extend across the economy or markets. The key issues will differ from country to country. We see the Australia’s DC super system as overall beneficial and an unlikely propagator of system stress. We trust that its features may provide some useful lessons for other systems.

*David Bell is executive director, and Geoff Warren is research fellow at The Conexus Institute, an independent think-tank philanthropically funded by Conexus Financial, publisher of Top1000funds.com

Leave a Comment

You must be logged in to post a comment.

Login