New PRI chief outlines priorities

In his first interview as the new CEO of the PRI, David Atkin outlines his priorities for the organisation and the areas of urgency for investors focused on sustainability

In his first interview as the new CEO of the PRI, David Atkin outlines his priorities for the organisation and the areas of urgency for investors focused on sustainability

Australia’s largest superannuation fund, the A$250 billion AustralianSuper, plans to decrease its equity allocation in favour of fixed income according to the fund’s CIO Mark Delaney, as he predicts central banks will tap the brakes on monetary policy amid concerns of rising inflation.

The largest sovereign wealth fund in the world, Norway’s Government Pension Fund Global, resembles an index fund and is not making the most of its tracking error boundaries according to a review of the active management of the fund by a team of specialists who recommended more clarity of mandate.

The CIO of Canada Pension Plan Investments, Edwin Cass, shares insights on the benefits of leverage, the impact on liquidity and the governance structures for success.

Giant Dutch pension provider, PGGM, has been a leader in embracing 3D portfolios shaped around risk, return and impact. Top1000funds.com talks to Piet Klop the new head of responsible investment about the journey so far and what is next in linking the portfolio to positive real-world outcomes.

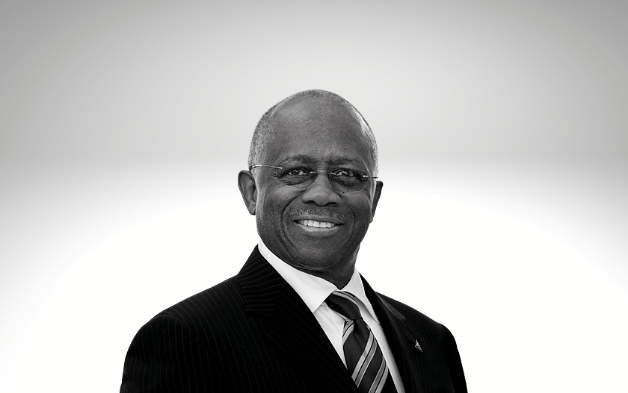

Henry Jones, who will resign as president of the CalPERS board on January 21, leaves behind a new mindset at the fund of tackling big systemic issues including sustainability and racism.

Top1000funds.com is the market leading news and analysis site for the world’s largest institutional investors. It focuses on leading the global investment industry to continuous improvement through case studies of best practice in governance and decision making, portfolio construction and efficient portfolio management, fees and costs, and sustainable investing.

The publication pushes the industry to question whether status quo processes and behaviours to tackle risks and opportunities will be sufficient in the future, and actively campaigns for diversity, sustainability, transparency, innovation and better alignment of fees in the investment industry.

Top1000funds.com is read by investment professionals in more than 40 countries.