How the Future Fund found agility

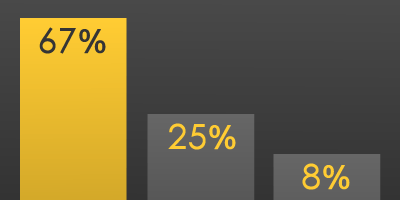

Using a fund of funds enabled the Future Fund to build a large exposure to hedge funds quickly during the global financial crisis.

Using a fund of funds enabled the Future Fund to build a large exposure to hedge funds quickly during the global financial crisis.

In this paper, Steven Kaplan from the University of Chicago Booth School of Business and National Bureau of Economic Research considers the evidence for three common perceptions of US chief executive officer pay and corporate governance. The first is that chief executive officers are overpaid and their pay keeps increasing; the second is that CEOs … Read more

Active quant strategies came in for criticism after the global financial crisis, with a number of models seen as lacking both the appropriate diversification and the dynamism necessary to react to major market events. While acknowledging the need to rethink quant models, global head of active equities for developed markets at State Street Global Advisor … Read more

As British Columbia Investment Management Corporation (BCIMC) moves towards its target of having 30 per cent of its portfolio exposed to real assets, it is seeking collaborative opportunities with similar large institutional investors. The investment manager is on the lookout for other like-minded investors and has already made significant co-investments in recent years. This year … Read more

Global pension funds continue to have a defensive asset allocation, reflected in the anaemic growth in the total assets of the world’s largest 300 pension funds by less than 2 per cent in 2011, new Towers Watson research reveals. The P&I/ Towers Watson Global 300 research reveals that concerns about ongoing uncertainty in global markets … Read more

Top1000funds.com is the market leading news and analysis site for the world’s largest institutional investors. It focuses on leading the global investment industry to continuous improvement through case studies of best practice in governance and decision making, portfolio construction and efficient portfolio management, fees and costs, and sustainable investing.

The publication pushes the industry to question whether status quo processes and behaviours to tackle risks and opportunities will be sufficient in the future, and actively campaigns for diversity, sustainability, transparency, innovation and better alignment of fees in the investment industry.

Top1000funds.com is read by investment professionals in more than 40 countries.