How to fix a broken labour market

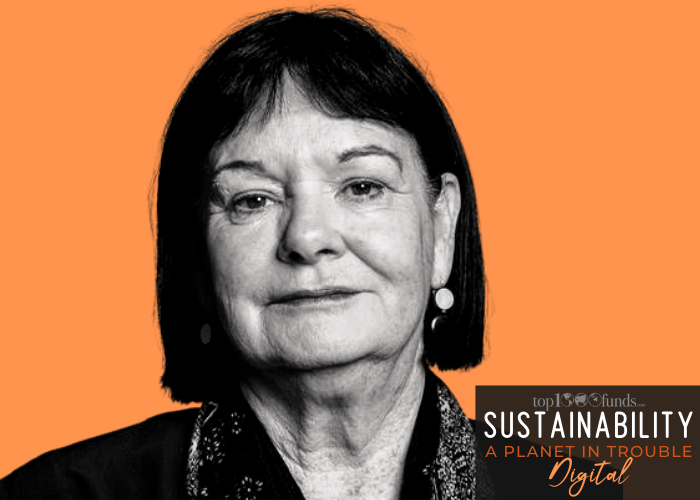

In an impassioned call Sharan Burrow, general secretary of the ITUC which represents 200 million workers in 163 countries called on institutional investors to do more to protect workers rights.

In an impassioned call Sharan Burrow, general secretary of the ITUC which represents 200 million workers in 163 countries called on institutional investors to do more to protect workers rights.

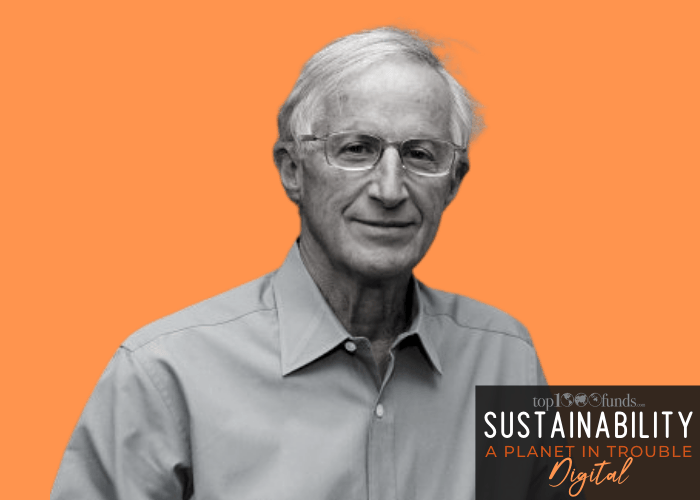

Nobel Prize winner Professor William Nordhaus, Sterling Professor of Economics and Professor of Forestry and Environmental Studies at Yale University, explains his theory of ‘No Regrets’ whereby companies can integrate ESG at a level that brings real benefits for society but has limited impact on the corporate.

Two of the world’s most influential institutional investors are hitting a brick wall in their attempts to engage with Amazon’s board on workplace safety. Every time the Netherland’s APG and the office of New York City Comptroller, fiduciary to New York city’s five pension funds, try to engage with the board at the tech giant in which they own a combined $6.5 billion they get push back from management.

Investors from Brunel, Wespath and Robeco talk about the challenges of shaping their net zero portfolios including data, benchmarks and holding managers to account.

Sustainability bonds issued by sovereign governments in developing and emerging markets offer exciting investor opportunities. The proceeds are used for impact and allow investors to target real change in sectors like health and education. Emerging market specialists describe how it could be the missing link to the ESG jigsaw.

Targets, allocating to diverse managers and acting on calls for change from diverse staffers are just some of the ways asset owners are boosting diversity in their own organisations. Investors at the Kresge Foundation, AP2 and AIMCo talk about their diversity, equity and inclusion action.

Top1000funds.com is the market leading news and analysis site for the world’s largest institutional investors. It focuses on leading the global investment industry to continuous improvement through case studies of best practice in governance and decision making, portfolio construction and efficient portfolio management, fees and costs, and sustainable investing.

The publication pushes the industry to question whether status quo processes and behaviours to tackle risks and opportunities will be sufficient in the future, and actively campaigns for diversity, sustainability, transparency, innovation and better alignment of fees in the investment industry.

Top1000funds.com is read by investment professionals in more than 40 countries.