Does ‘ESG’ spell ‘Embellished Shiny Grading’?

Is hyper focus on sustainable investing reminiscent of previous bubbles?

Is hyper focus on sustainable investing reminiscent of previous bubbles?

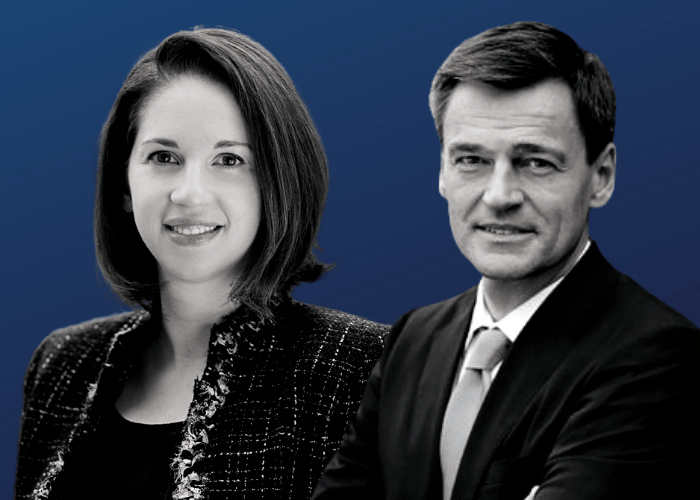

The appointment of Karen Karniol-Tambour and Carsten Stendevad as co-CIOs of Bridgewater’s new sustainability business marks a major milestone in the hedge fund’s business, applying its deep research-driven systematic approach to a new set of problems. Amanda White speaks exclusively to the two CIOs.

Investors all over the world are pondering the inflationary environment. Is inflation coming? Will it stick? What does it mean for investments? Is stagflation possible and how should portfolios be hedged? The Fiduciary Investors Symposium will take a deep dive into the inflationary expectations of investors and look to history as a guide on asset class performance during different inflationary regimes.

Research conducted by Scientific Beta looks at the performance of ESG strategies and asks whether non-financial information in ESG scores offers additional performance benefits. The research finds that the effect of risk adjusting the performance of ESG strategies shrinks the apparent alpha to a level where none of the strategies delivers positive alpha.

Road to 2030 is a thematic project designed to highlight undiscounted change. We believe that understanding the key long-term structural thematic drivers is the basis of good investment thinking.

Who is racing ahead in the EV transition? Passenger cars have got a head start, but trucks – responsible for 8% of global GHG emissions – are key drivers in the journey to net zero.

Top1000funds.com is the market leading news and analysis site for the world’s largest institutional investors. It focuses on leading the global investment industry to continuous improvement through case studies of best practice in governance and decision making, portfolio construction and efficient portfolio management, fees and costs, and sustainable investing.

The publication pushes the industry to question whether status quo processes and behaviours to tackle risks and opportunities will be sufficient in the future, and actively campaigns for diversity, sustainability, transparency, innovation and better alignment of fees in the investment industry.

Top1000funds.com is read by investment professionals in more than 40 countries.